Decide if homeownership is right for you with the CalcGami Rent vs Buy Calculator. Compare the long-term wealth impact of renting versus buying a home in the USA. Analyze down payments, appreciation, tax benefits, and maintenance costs. Save your scenarios and share results via WhatsApp.

10-Year Financial Winner

Ready

Compare your options to see which saves you more money.

Total Cost to Buy

$0

Includes Equity & Appreciation

Total Cost to Rent

$0

Includes Lost Investment Gains

Saved Comparisons

| Date | Home Price | Winner |

|---|

Table of Contents

What is a Rent vs Buy Calculator?

A Rent vs Buy Calculator is a powerful financial modeling tool designed to help individuals and families navigate one of the most significant life decisions in the American economy. In the United States, the “American Dream” is often tied to homeownership, but rising interest rates and high property values have made the choice between renting and buying more complex than ever before.

This calculator performs a side-by-side comparison of the total cost of renting a property versus the total cost of buying a home over a specific period. It goes beyond just comparing a monthly rent check to a mortgage payment. A true “Rent vs Buy” analysis accounts for Sunk Costs (money you never see again), such as property taxes, maintenance, homeowners insurance, and mortgage interest, as well as Opportunity Costs (what you could have earned by investing your down payment in the stock market instead).

Whether you are looking at a condo in a major city or a single-family home in the suburbs, this calculator provides a data-driven answer to which path builds more wealth. It features History to compare different zip codes, Save Calculation to log specific property addresses, and WhatsApp Share to discuss the results with your spouse or real estate agent.

Benefits of Using a Rent vs Buy Calculator

Making this decision based on “gut feeling” can lead to massive financial regret. Using a calculator provides several strategic benefits:

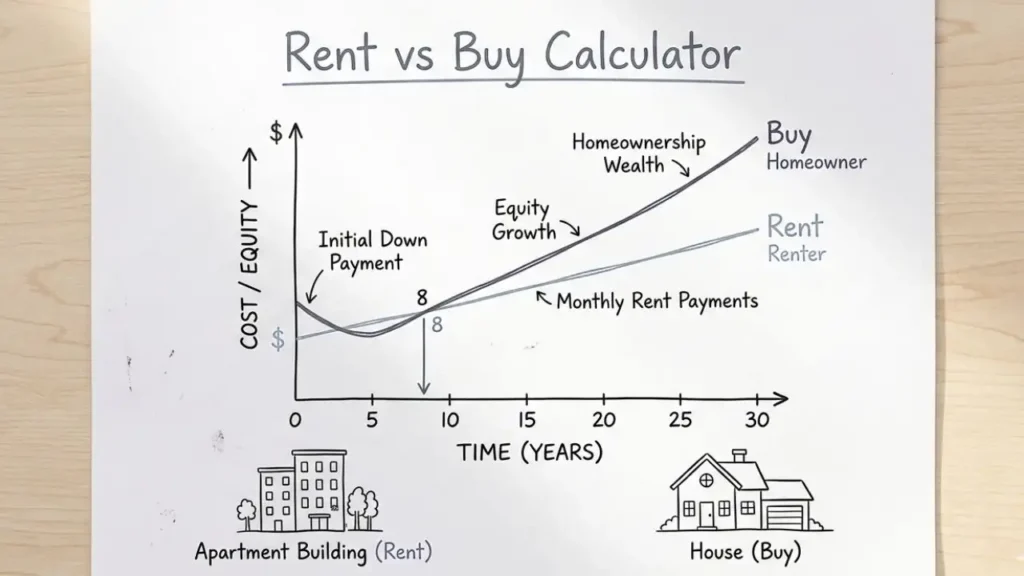

- Understanding the “5-Year Rule”: Generally, in the USA, if you plan to move in less than five years, renting is often cheaper due to the high closing costs (6%–10% of the home value) associated with buying and selling. This tool proves exactly when your “Break-Even Point” occurs.

- Tax Advantage Analysis: Homeowners in the USA may benefit from the Mortgage Interest Deduction and property tax deductions (up to the SALT limit). The calculator helps you see if these tax breaks actually move the needle for your specific income level.

- The Power of Appreciation: Real estate in the USA historically appreciates over time. This tool allows you to input an expected annual growth rate (e.g., 3%) to see how much equity you could build over 10 or 20 years.

- Factoring in Maintenance: A common mistake is forgetting that “rent is the maximum you pay, but a mortgage is the minimum you pay.” This tool includes a “Maintenance Factor” (usually 1% of the home value per year) to give you a realistic view of homeownership costs.

- Opportunity Cost Tracking: If you have $50,000 for a down payment, what happens if you invest that in an S&P 500 index fund instead of a house? This calculator compares the growth of your down payment vs. the growth of home equity.

- Collaborative Planning: Use WhatsApp Share to send the final “Winner” (Rent vs Buy) to your partner so you can align on your 10-year financial goals.

Formula Used in Rent vs Buy Calculator

The Rent vs Buy Calculator compares the Net Future Value of both options after a set number of years.

The Plain Text Formulas:

- Total Cost of Renting:

Formula: (Monthly Rent x Months) + (Renter’s Insurance x Months) – (Investment Return on Down Payment) - Total Cost of Buying:

Formula: (Mortgage Payments) + (Closing Costs) + (Maintenance) + (Property Taxes) – (Home Appreciation) – (Principal Paydown) + (Selling Costs)

How to Use the Rent vs Buy Calculator

Follow these steps to find your financial break-even point:

- Enter Home Details: Input the purchase price of the home you are considering.

- Enter Rent Details: Input the monthly rent for a similar property in that area.

- Enter Loan Details: Input your down payment and current mortgage interest rate.

- Enter Duration: Select how many years you plan to stay in the home (e.g., 7 years).

- Enter Financial Assumptions: Input estimated annual home appreciation (3% is standard) and investment returns (7% for stocks).

- Calculate: See which option results in a higher net worth.

- Use Productivity Features:

- History: Compare a home in Florida (low tax) vs. New Jersey (high tax).

- Save Calculation: Store as “123 Maple St – Buying Scenario.”

- Share on WhatsApp: Send: “Based on our 7-year plan, buying this house will save us $25,000 over renting!”

Real-Life Example

The Scenario:

Imagine you are choosing between renting an apartment for 2,500/month or buying a house for 400,000. You plan to stay for 7 years.

The Details:

- Rent: $2,500/month (increasing 3% annually)

- Buy: $400,000 Home (5% down, 6.5% interest)

- Appreciation: 3% per year

The Calculation:

- Total Cost to Rent: Over 7 years, you spend $228,000 in rent.

- Total Cost to Buy: After accounting for interest, taxes, and selling fees, but adding back your $92,000 in equity and appreciation.

- The Difference: Buying results in a net gain of $18,000 compared to renting.

The Result:

Buying is the winner by $18,000.

Action: You save this as “7-Year Plan” and use WhatsApp Share to show your spouse that buying makes sense if you commit to staying at least 7 years.

Frequently Asked Questions (FAQ)

What is the “Price-to-Rent Ratio”?

This is a quick way to gauge a market. Divide the home price by the annual rent. A ratio under 15 usually favors buying; a ratio over 20 usually favors renting. Our calculator does a much deeper dive than this simple ratio.

Is it true that “renting is throwing money away”?

Not necessarily. While rent is a “sunk cost,” so is mortgage interest, property tax, and homeowners insurance. In the first few years of a mortgage, almost 80% of your payment is interest (sunk cost). Renting can be a smarter financial move if you value flexibility or if the local housing market is overvalued.

How does the “Standard Deduction” affect this?

In the USA, the standard deduction is quite high (currently over $29,000 for married couples). Many homeowners find that their mortgage interest doesn’t exceed this amount, meaning they don’t get an extra “tax break” for buying. This calculator helps you see the reality of your specific tax situation.

Should I include maintenance in the calculation?

Absolutely. As a homeowner, you are responsible for the roof, HVAC, plumbing, and landscaping. A safe estimate is to set aside 1% of the home’s value per year for maintenance. If you buy a $400,000 home, that is $4,000 a year you wouldn’t spend while renting.

What are “Closing Costs”?

When you buy a home, you typically pay 2%–3% of the price in fees (inspections, title insurance, loan origination). When you sell, you pay roughly 6% in realtor commissions. These “entry and exit” fees are why buying is usually only profitable if you stay for several years.

How does inflation affect renting vs. buying?

Buying acts as a “hedge” against inflation. While your landlord can raise your rent every year, a Fixed-Rate Mortgage stays the same for 30 years. Over time, your housing cost as a percentage of your income usually drops if you buy.

What if the housing market crashes?

If home prices drop, renting is the safer option as you have no equity to lose. However, the US housing market has historically increased in value over any 10-year period. You can use the calculator to test a “0% appreciation” scenario to see the worst-case result of buying.

Can I use this for a Condo vs. Apartment?

Yes. If calculating for a condo, make sure to include the HOA (Homeowners Association) fees in the “Monthly Costs” section, as these can be a significant recurring expense that renters don’t have to worry about.