Boost your FICO score with the CalcGami Credit Utilization Calculator. Instantly determine your debt-to-limit ratio to optimize your credit health in the USA. Save your balances, track your progress toward the 30% rule, and share credit-building tips via WhatsApp.

Total Credit Utilization

0%

Add your card balances to check your ratio.

Total Balances

$0.00

Total Credit Limit

$0.00

History

| Date | Total Balance | Ratio |

|---|

Table of Contents

What is a Credit Utilization Calculator?

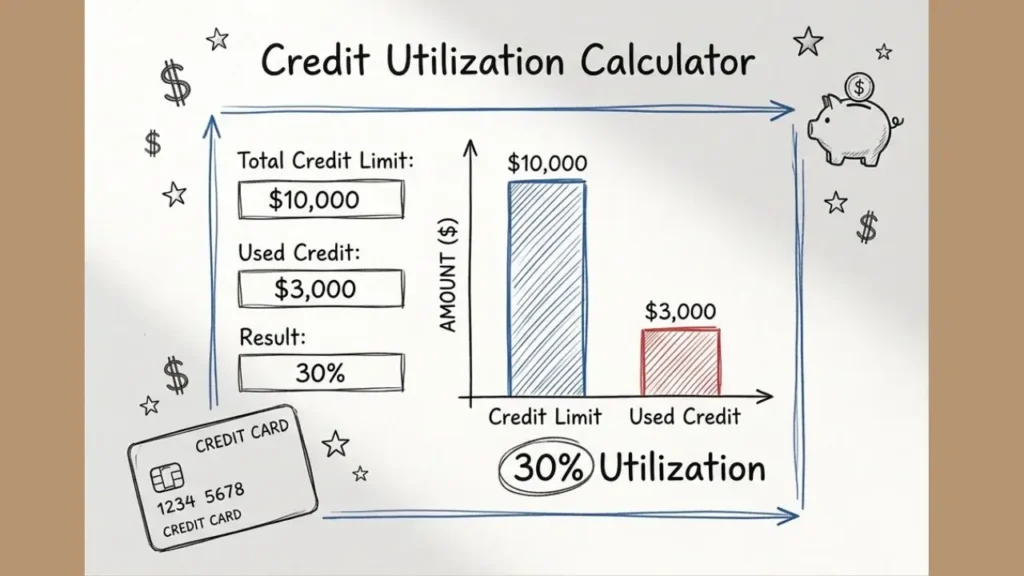

A Credit Utilization Calculator is a strategic financial tool designed to measure your “revolving credit” health. In the United States, your Credit Utilization Ratio is the second most important factor in determining your FICO score, accounting for a massive 30% of your total credit rating. Simply put, it is the percentage of your total available credit that you are currently using.

Lenders in the USA use this ratio to gauge how “thirsty” you are for debt. If you have a $10,000 credit limit and you have spent $9,000, you are 90% utilized, a major red flag that indicates financial stress. Conversely, keeping that balance low shows you are a responsible borrower. This calculator automates the math for you.

By entering your Current Balances and Total Credit Limits across all your cards, it provides an instant percentage. It features History to monitor your debt-reduction journey, Save Calculation to log your monthly statement changes, and WhatsApp Share to update your spouse or financial advisor on your progress toward a better score.

Benefits of Using a Credit Utilization Calculator

In the competitive American credit landscape, understanding this single number can be the difference between a loan approval and a rejection. This tool provides several high-value benefits:

- The Fastest Way to Raise Your Score: Unlike “Payment History,” which takes months of consistency to improve, lowering your utilization can boost your credit score in as little as 30 days. This calculator helps you see exactly how much you need to pay off to hit your target score.

- Identify High-Risk Cards: Sometimes one “maxed-out” card can hurt your score even if your other cards have zero balances. Use the tool to identify which individual card is dragging down your average.

- Target the “30% Rule”: Financial experts in the USA generally recommend keeping your utilization under 30%. This calculator acts as a “speedometer,” warning you when you are entering the “danger zone” of high utilization.

- Prepare for Major Purchases: If you are planning to buy a home or car in 2026, use this tool three months in advance to optimize your ratios and secure the lowest possible interest rates.

- Strategic Credit Limit Increases: If you can’t pay down your debt immediately, the calculator can show you how much of a Credit Limit Increase you should request from your bank to artificially lower your ratio.

- Accountability and Sharing: Use WhatsApp Share to send your current ratio to your debt-payoff partner, ensuring you both stay committed to your financial goals.

Formula Used in Credit Utilization Calculator

The calculator uses a simple but powerful ratio formula to determine your standing with the credit bureaus.

Formulas:

- Individual Card Utilization:

Formula: (Balance on One Card / Limit of That Card) x 100 = Individual % - Total Aggregate Utilization:

Formula: (Sum of All Balances / Sum of All Limits) x 100 = Total %

How to Use the Credit Utilization Calculator

Follow these steps to get an accurate view of your revolving debt:

- Gather Your Statements: Open your latest credit card apps (e.g., Amex, Chase, Citi).

- Enter Your Balances: Input the “Current Balance” for each of your revolving credit cards.

- Enter Your Limits: Input the “Total Credit Limit” for each card.

- Add Multiple Cards: Use the “+” button to include all your active accounts.

- Calculate: View your total aggregate utilization percentage.

- Use Productivity Features:

- History: Compare your utilization from January vs. June.

- Save Calculation: Store as “June 2026 Credit Check.”

- Share on WhatsApp: Send: “I finally got my credit utilization down to 15%!”

Real-Life Example

The Scenario:

Imagine you have two credit cards. Card A has a 2,000 balance with a 5,000 limit. Card B has a 500 balance with a 5,000 limit. You want to know your total utilization.

The Details:

- Total Balances:

2,500(2,500(2,000 + $500) - Total Limits:

10,000(10,000(5,000 + $5,000)

The Calculation:

- Divide Balance by Limit: $2,500 / $10,000 = 0.25

- Convert to Percentage: 0.25 x 100 = 25%

The Result:

Your total credit utilization is 25%.

Action: You save this as “Current Standing” and use WhatsApp Share to show your financial coach that you are safely under the 30% threshold.

Frequently Asked Questions (FAQ)

What is the “ideal” credit utilization percentage?

While 30% is the standard recommendation, those with the highest credit scores (800+) typically keep their utilization under 10%. The lower your ratio, the more “points” you earn in the FICO model.

Does 0% utilization help my score?

Surprisingly, having 1% utilization is often better than 0%. Lenders like to see that you are actually using your credit but managing it perfectly. If you have 0% across every single card, the algorithm might view you as “inactive.”

Should I close a credit card I’m not using?

Usually, no. Closing a card reduces your Total Credit Limit. If you have a balance on other cards, closing an unused card will cause your utilization ratio to jump instantly, which will lower your credit score.

When do credit card companies report to the bureaus?

Most banks report your balance once a month on your Statement Closing Date. If you pay off your card after the statement is generated, your high balance might still be reported to Experian, Equifax, and TransUnion for that month.

Is it better to pay off one card completely or spread it out?

Both “Individual” and “Aggregate” utilization matter. It is generally better to pay off a “maxed-out” card completely first to eliminate the 90%+ red flag on that specific account, then focus on lowering the total average.

Do my debit card or personal loans count toward this?

No. Credit utilization only applies to Revolving Credit (credit cards and lines of credit). Installment loans like car payments, mortgages, or student loans are calculated differently and do not affect this specific ratio.

How fast will my score change after I lower my utilization?

No. Credit utilization only applies to Revolving Credit (credit cards and lines of credit). Installment loans like car payments, mortgages, or student loans are calculated differently and do not affect this specific ratio.

Can I use this for my business credit cards?

In the USA, most business credit cards do not report to your personal credit report unless you default. However, some (like Capital One Spark) do report. Check your card’s terms to see if it impacts your personal utilization ratio.