Predict your financial future with the CalcGami Credit Score Estimator. Understand how your payment history, credit utilization, and debt levels impact your FICO and VantageScore in the USA. Save your progress and share credit-building tips via WhatsApp.

Estimated Credit Score

---

Select your details to calculate an estimate.

Rating Category

Pending

Loan Eligibility

Unknown

Recent Estimates

| Date | Score | Rating |

|---|

Table of Contents

What is a Credit Score Estimator?

A Credit Score Estimator is a predictive financial tool designed to help Americans understand the “why” behind their credit rating. In the United States, your credit score is essentially your “financial GPA.” It dictates whether you can buy a home, lease a car, or even get a specific job. Unlike a formal credit report, which shows your past behavior, an estimator allows you to look forward and simulate how future actions, like paying off a debt or opening a new card, will impact your score.

Most credit scores in the USA are calculated using either the FICO model or the VantageScore model. These scores range from 300 to 850, and while the exact algorithms are proprietary secrets, they are all based on five core pillars of data. This calculator uses those weighted pillars to estimate your current standing.

Whether you are recovering from a financial setback or trying to reach the elite “800 Club,” this estimator provides the roadmap you need. It features History to track your score’s upward trend, Save Calculation to log your monthly progress, and WhatsApp Share to send credit-building strategies to your family or financial coach.

Benefits of Using a Credit Score Estimator

In a country where “Credit is King,” knowing your estimated score is the first step toward significant savings. Using this tool offers several key advantages:

- Lower Interest Rates: A “Good” score (700+) versus a “Fair” score (640) can save you over $100,000 in interest over the life of a 30-year mortgage.

- Approval Confidence: Before you apply for a new credit card or auto loan, use the estimator to see if you are likely to be approved. This prevents unnecessary “Hard Inquiries” that can temporarily lower your score.

- Strategic Debt Repayment: See the massive impact of lowering your Credit Utilization Ratio. Often, paying down a credit card balance to below 30% of its limit provides the fastest score boost.

- Rental and Utility Perks: Landlords and utility companies in the USA use credit scores to determine security deposits. A higher score often means you can move into a new apartment with $0 down.

- Insurance Premium Savings: In many US states, auto and homeowners insurance companies use “Credit-Based Insurance Scores” to set your rates. Improving your score can literally lower your monthly bills.

- Financial Literacy: Use WhatsApp Share to educate your children or siblings on how credit works, helping the next generation start their financial lives with a “Good” score.

Logic Used in Credit Score Estimator

While the exact math is complex, the US credit model (FICO) is based on these five weighted categories:

The Weighted Pillars:

- Payment History (35%): Do you pay your bills on time? This is the single most important factor.

- Amounts Owed / Utilization (30%): How much of your available credit are you using? (Goal: Stay under 30%).

- Length of Credit History (15%): How long have your accounts been open? (Older is better).

- Credit Mix (10%): Do you have a variety of credit (e.g., a credit card, a car loan, and a mortgage)?

- New Credit (10%): How many accounts have you opened recently? (Too many “Hard Pulls” is a red flag).

How to Use the Credit Score Estimator

Follow these steps to get a realistic view of your credit health:

- Input Payment History: Indicate if you have had any late payments in the last 7 years.

- Enter Total Debt vs. Credit Limits: Input your current balances compared to your total available credit (Utilization).

- Enter Age of Accounts: Input the age of your oldest active credit account.

- List Recent Inquiries: Input how many times you have applied for credit in the last 6 months.

- Calculate: View your estimated score range (e.g., 680–720).

- Use Productivity Features:

- History: See how your score has improved since you started paying off debt.

- Save Calculation: Store as “May 2026 – Pre-Mortgage Check.”

- Share on WhatsApp: Send: “My estimated credit score is finally in the 700s!”

Real-Life Example

The Scenario:

“Alex” has a 5,000 limit on his credit card but is currently carrying a 4,500 balance (90% utilization). His current estimated score is 640. He wants to see what happens if he pays the balance down to $1,000.

The Details:

- Old Utilization: 90% ($4,500 / $5,000)

- New Utilization: 20% ($1,000 / $5,000)

- Action: Paying off $3,500 of debt.

The Calculation:

- Utilization Drop: From 90% to 20%.

- Point Gain: Dropping below 30% utilization typically yields a 40–80 point boost.

The Result:

Alex’s estimated score jumps from 640 to 710.

Action: Alex saves this result and uses WhatsApp Share to tell his wife that they are now in the “Good Credit” range to apply for a better car loan rate.

Frequently Asked Questions (FAQ)

Is this estimator a “Hard Pull” on my credit?

No. Using an estimator is a “Soft Inquiry” or a simulation. It does not communicate with the credit bureaus (Equifax, Experian, TransUnion) and therefore will not lower your score.

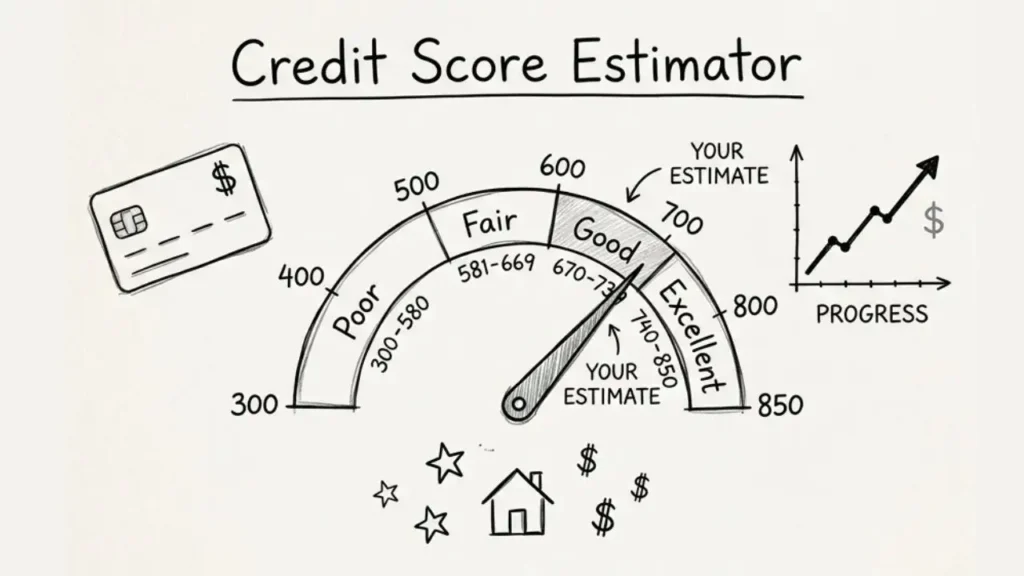

What is a “Good” credit score in the USA?

Generally, scores are categorized as:

Exceptional: 800–850

Very Good: 740–799

Good: 670–739

Fair: 580–669

Poor: 300–579

How fast can I raise my credit score?

If your score is low due to high utilization, you can see a jump in as little as 30 days once the credit card company reports your lower balance. If your score is low due to late payments, it takes longer (consistently on-time payments over 6–12 months).

Do debit cards help my credit score?

No. In the USA, debit cards use your own money from a checking account. Since no money is being “borrowed,” no data is reported to the credit bureaus. To build credit, you need a credit card or a loan.

Should I close my old credit cards?

Usually, no. 15% of your score is based on the Length of Credit History. Closing an old card can shorten your average account age and lower your score. It is often better to keep it open with a $0 balance.

What is “Credit Utilization” and why does it matter?

It is the percentage of your total credit limit that you are actually using. Lenders view people who max out their cards as “high risk.” Keeping your utilization under 10% is the secret to reaching the 800+ score range.

How long do negative marks stay on my report?

Most negative information, like late payments or collections, stays on your US credit report for 7 years. Bankruptcies can stay for up to 10 years.

Can I use this for my business credit score?

This tool is specifically for Consumer Credit Scores. Business credit scores (like the Dun & Bradstreet PAYDEX score) use different criteria, focusing primarily on how quickly you pay your vendors and suppliers.